What’s the difference between

Both come from notionally democratic republics. Both come from a Treasury with the power to create money. Both come from areas with excess deaths due to the wide prevelance of gun ownership.

On the face of it the latter instrument is better, since it has a bigger number printed on it. As MMT’ers often say, anybody can create money. The trick is getting somebody else to accept it.

In this case, the point of the exercise is to gain a credit in the Treasury General Account (TGA) at the US Federal Reserve. So what will the Fed offer for these two tokens, and why?

What is a bank?

At its core a bank is a fairly simple operation. It takes something physical of value and creates an amount of its own liabilities in return. So a mortgage, despite common belief, isn’t a loan; it’s the charge over the property. That is what the bank has created as a financial derivative of a property and which the bank owns as security for the liabilities it has issued against that charge. The property owner is then given a schedule by which they can buy back that charge over time. Once that is complete the mortgage is ‘discharged’.

The bank won’t offer the full price of the property in return for the charge. Instead they will only give a smaller amount. This is known as the haircut. The difference between what you are given now, and the amount you have to give back to re-purchase the charge is known as the ‘discount’.

Thus banks make their money by taking or deriving collateral assets, giving them a haircut and discounting those assets into liabilities they create just for that purpose. The circulation of those liabilities is what we call ‘bank money’.

In essence a bank is a glorified pawnbroker that issues its own money to pawn items, rather than using money issued by somebody else.

Depositing coin

Given that banks make money from discounting, why would a bank ever offer the face value for a coin or a note? Generally they don’t quite. You get charged for depositing cash (or at least a large amount of cash) at a bank, and that fee is the bank’s discount. However the discount is usually small (I get charged £0.70 per £100).

The reason the bank is happy to take cash at near the face value is because they can sell it on for that face value and get a reserve credit at the central bank. The entity they can sell it back to is the Treasury that issued it.

Here in the UK coins are minted by the Royal Mint on the orders of HM Treasury. These are sold directly to the bank coin clearing system in return for transfer of bank reserves to HM Treasury. However HM Treasury stands ready to repay those coins on demand. There is a contigent liability listed in the Consolidated Fund accounts.

Should there be a sudden rush to get rid of coin, HM Treasury would have to pay out £4.6bn, which it can do easily at any time given that the UK has a ‘seigniorage’ clause in the legislation that allows HM Treasury to order the Bank of England to make the payment(1).

The problem in the USA is that the TGA isn’t fully elastic and the debt ceiling limit means it can’t go any further. Very quickly banks may start to feel that notes and coins are no longer exchangeable at face value from the Treasury for bank reserves.

What does this mean for The Coin

Certainly when presented with a Trillion Dollar Coin from a clearly fiscally constrained Treasury, the Federal Reserve may wish to consider a substantial haircut to manage its risk. That may be as severe as treating the coin as a lump of platinum bullion or, at best, as a novelty collectors token. So it may only issue a few dollars against it.

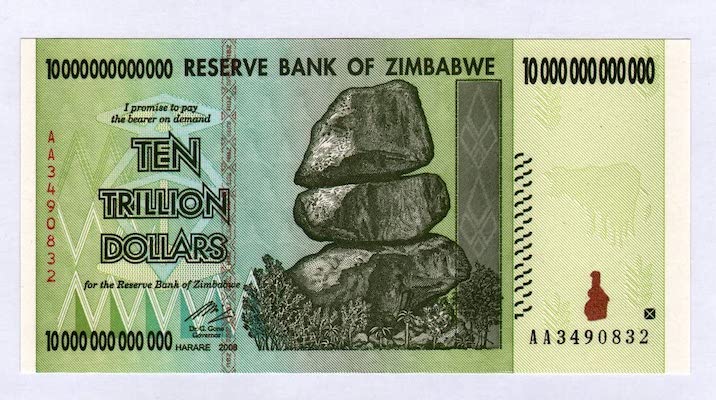

Much as it would if presented with a ten trillion dollar Zimbabwe note, and for the same reason. The Treasury behind it is broke.

There doesn’t appear to be a legal requirement for banks to take coin at face value. It happens because market forces push the value of the coin towards its face value - all due to faith that Treasury will swap their coin one-for-one for bank credit on demand.

“Legal tender” doesn’t help. Legal tender just says you can pay your debts in court with notes and coins. It says nothing about the acceptance of the currency in the normal course of business. Certainly nothing about acceptance at a bank, let alone the central bank. There is no creditor here discharging a debt.

Moreover if Treasury hits its debt ceiling it cannot redeem normal dollar notes and coins at face value, which could mean banks will stop accepting them for deposit, or start to discount them as they do with foreign notes and coins.

I wonder if those clinging to the debt ceiling limit have considered that they may inadvertently undermine the acceptibility of the physical currency within the financial system. All because they don’t understand how money works in a modern money economy.

Taxes to the rescue

It’s next to impossible to pay your taxes with cash in the UK now. However the US isn’t that far down the line. So if banks start seeing your notes and coins as a bit suspect, it is still worth full value for credit against US tax bills. Exactly as MMT explains.

(1). Coin redemption is a standing service and is repayable from the Consolidated Fund under s13 Exchequer and Audit Department Act 1866.