We’re not.

Here’s why Starmer’s Banana Bonds plan won’t raise a single extra penny for the government.

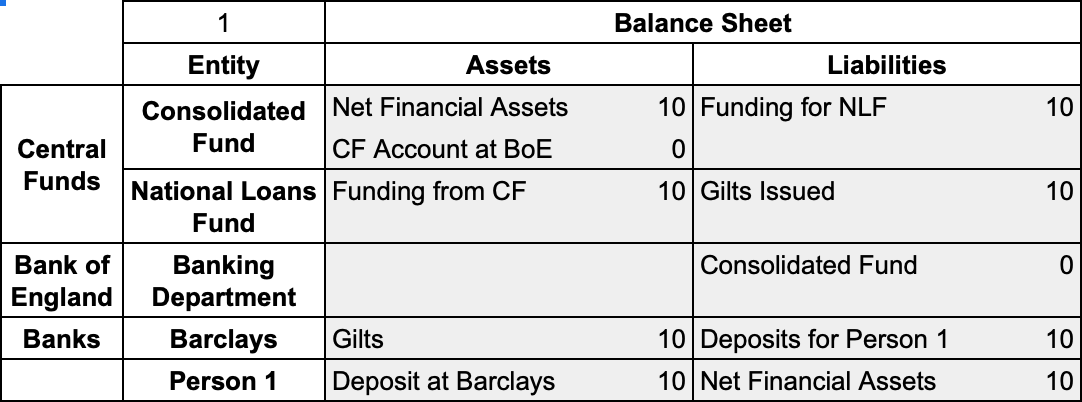

This is the end of day position after the government has added £10 to the economy via its spending.

Person 1 has brand new savings at Barclays and the Debt Management Office cash management process has ‘sterilised’ this money addition via a Gilt sale. (There is no need to do this, it is a matter of government policy - currently called the ‘full funding rule’. They could have been left as reserves.)

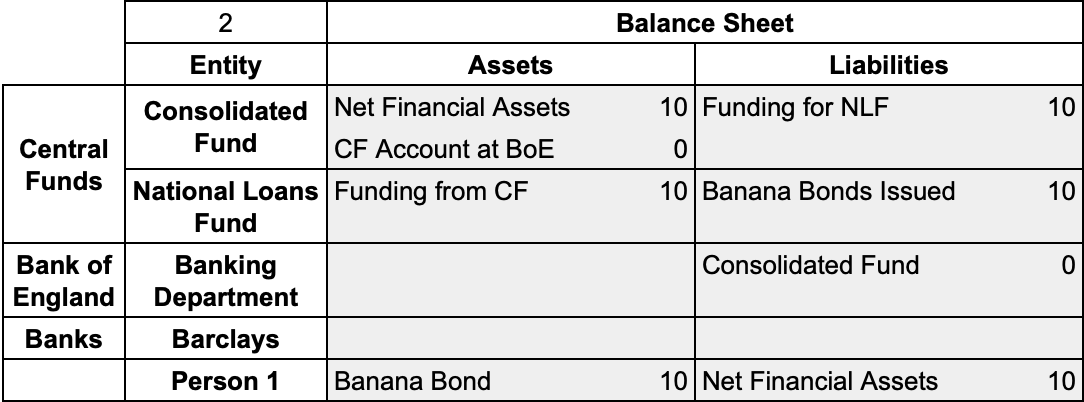

Now let’s show what happens when Person 1 uses their £10 to buy one of these magical bonds.

All that happens is the balance sheet of the commercial bank shrinks and a Gilt is swapped for a Banana Bond. Not one extra penny is added to the Consolidated Fund by the process.

Because, of course, money from the Consolidated Fund comes via votes in Parliament not by flogging cheap gimmicks to the public. If Starmer wants money for any project, all he has to do is put a Supply Estimate in and get Parliament to vote it through. And that funds the project. Each time, every time - in the same way it has been done for at least 150 years.

How is a Banana Bond somehow better than a savings deposit in Barclays? For anybody with less that £85K in the bank, who knows. Certainly there is no connection with accounting and legal reality.

Or it’s actually for people with more than £85K in the bank.

In which case why not just fix deposit protection so that all deposits in banks are fully secure?

We don’t need gimmicks. We need honesty. And a Job Guarantee.