We can use this process to model how the currencies flow from the point of view of a net exporter in a free floating currency rate environment.

For example, a Norwegian Bank contacts a UK bank and agrees to a contract to purchase 100 GBP for, say, 1158 NOK. That price is just agreed like any other price for a contract. The ‘exchange rate’ is just the banks shopping around between each other.

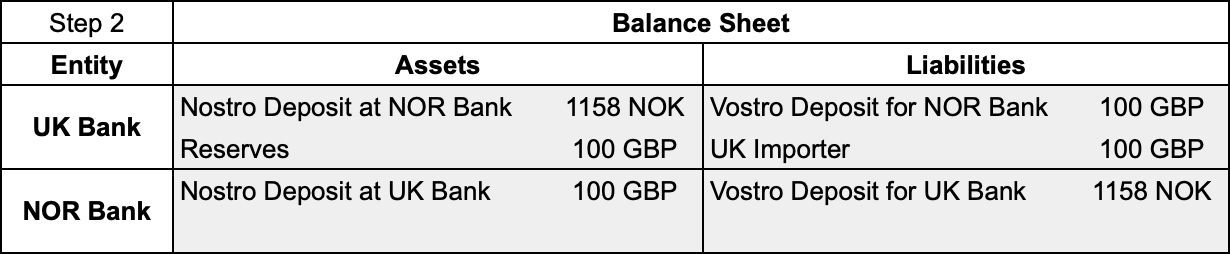

The Norwegian bank now has a contract from the UK Bank to credit it 100 GBP. The UK Bank similarly has a contract from the Norwegian Bank to credit it 1158 NOK

The Norwegian Bank takes the 100 GBP contract asset and discounts it to 1158 NOK on its books (marks up the liability out of nothing) and then credits the account of the UK Bank at the Norwegian bank with that 1158 NOK – fulfilling its side of the contract.

The UK Bank takes the 1158 NOK contract asset and discounts it to 100 GBP on its books (marks up the liability out of nothing) and then credits the account of the Norwegian bank at the UK Bank with that 100 GBP – fulfilling its side of the contract.

The contract assets are now replaced with deposit assets in the other bank. The Norwegian bank has an account with the UK Bank with 100 GBP in it and the UK Bank has an account with the Norwegian Bank with 1158 NOK in it. The balance sheets all balance.

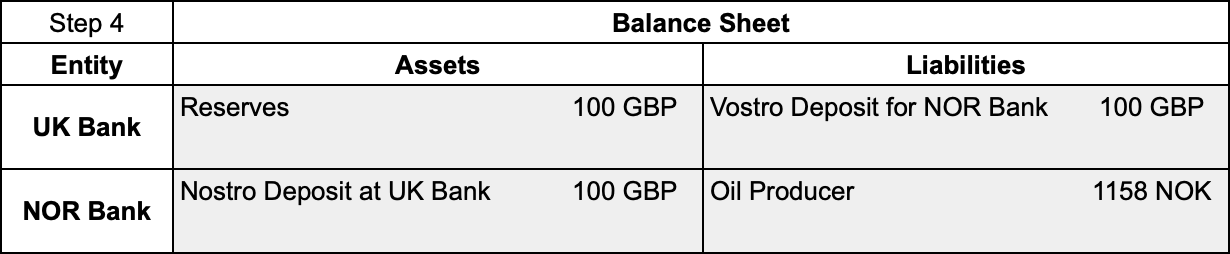

A UK importer hands over their 100 GBP and asks their bank to pay a Norwegian producer for a consignment of oil. The UK Bank deletes the (additional) 100 GBP deposit the UK importer holds and then contacts the Norwegian bank and asks them to transfer the 1158 NOK to the credit of the oil producer.

The result is a Norwegian Bank with a 100 GBP deposit, who gets a statement from the UK bank showing which account their pounds are in.

Note that either the Oil importer in the UK does the FX, or the oil supplier in Norway does the FX. Either way it has to be done to pay people in Norway, who want to receive NOK, not GBP. Similarly although oil may be priced in USD, the transaction here is GBP to NOK. That’s because customers desire to pay in the currency they have and suppliers desire to receive the currency they wish to hold. The financial system gets paid to make that desire a reality and selling in a local currency increases sales. The currency something is priced in isn’t necessarily the one it is invoiced in, or settled in - at either end of the deal.

The Oil Producer pays their staff, their suppliers and their investors in NOK.

The Norwegian state then taxes those flows in NOK as they bounce around the economy. Let’s assume the Norwegians are in a spending mood and over a series of transactions all the money becomes taxation.

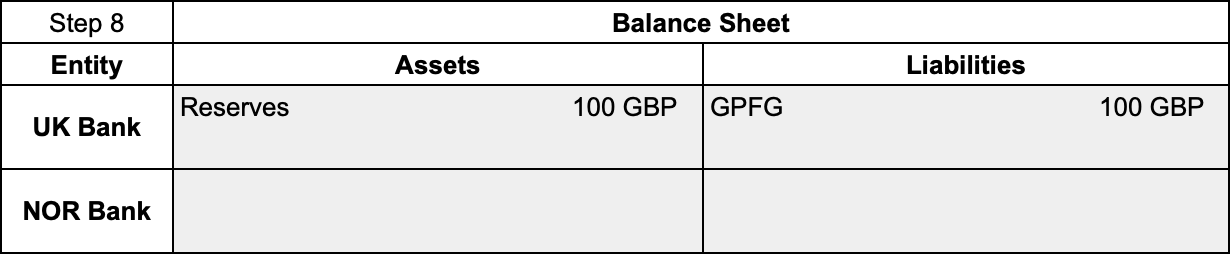

The policy of the Norwegian government is to pass onto the Government Pension Fund Global (GPFG) taxation arising from oil. (For convenience here assume that GPFG has an account at this particular NOR Bank. In reality there would be a set of inter bank NOK transfers to and from the Norges Bank where the GPFG and Skatteetaten hold their main accounts that would add nothing other than length to this post).

The GPFG then buys the 100 GBP deposit from the NOR Bank - relieving it of the currency risk

The net result is that the GBP deposit that was originally in the hands of a UK oil importer ends up, by a very circuitous route, in the hands of the Norwegian Government Pension Fund Global - ready to purchase UK financial assets.

And that is how a net exporter injects its own currency into its economy - via a touch of financial alchemy. The GPFG drains excess foreign currency from the Norwegian banking system and the Norwegian banks know that so are happier facilitating foreign transactions.

This process is common to all net exporters and comes in various forms from outright currency pegs where the central bank relieves the local banking system of its currency risk directly to leaving the banks to fend for themselves which tends to cause a drift towards ‘hard currencies’ - primarily the US dollar - that the banks are happy to hold as backing assets on their individual balance sheets for the local currency liabilities they issue against them.

What we can see is that although the process starts as money creation, the desire to get rid of currency risk pares that back to a simple exchange of savings. Somebody within the net exporter currency area has to end up as the saver of FX financial assets, and they are forced to be that entity or the currency rates will move to match the flow with the available quantity of savers. A currency rate move would be to strengthen the export currency and weaken the import currency - which destroys exports and therefore jobs in the exporting nation. The importing nation ends up with less stuff.

The choice, however, rests with the exporting nation - since they can bring their currency down by market intervention without limit. A smart importing nation would realise that and manage its relationships so that economic and political pressure in the export nation is brought to bear - rather than trying to buy foreign savers with needless interest payments. An approach that just exacerbates the problem rather than alleviates it - since the interest payment really needs to be saved.